What the heck does all this talk about LVR mean?

There’s lots of talk at the moment about the APRA (Australian Prudential Regulation Authority) tightening lending standards and lenders reducing the maximum LVR on new and interest-only lending, but do you know what the heck it all means? You can learn more about APRA’s announcement here. But, moving on, let’s start at the beginning… what is LVR?

Loan to value ratio (LVR) is calculated by dividing the amount of your home loan by the purchase price (or appraised value) of the property. Lenders then use this figure (your LVR) to gauge how risky it would be to give you a loan.

Loan to Value Ratio is calculated by dividing the loan amount by the actual purchase price or

valuation of the property, then multiplying it by 100.

For example, let’s say that you’d like to borrow $600,000 and the property that the applicant is using as security is valued at $750,000.

The LVR of the home loan would be calculated like this:

($600,000 loan ÷ $750,000 property value) x 100 = 80% LVR

Note: If the purchase price is different to the valuation then the lender and their mortgage insurer will use the lower of the two to determine the LVR.

According to ASIC’s Money Smart, ‘In general, the higher your LVR, the higher the risk the lender will not be repaid if you default on the loan and they have to sell the property. Having a high LVR may also affect your ability to refinance your loan later on, and you may have to pay mortgage

insurance again if the LVR on the new loan is high.

Usually lender’s mortgage insurance (LMI) is payable if your LVR is above 80%. This is a one-off insurance premium to protect the lender should you default on your home loan.

Some lenders also use your LVR to work out the interest rate on your home loan. For example, if your LVR is more than 80%, you could be charged a higher interest rate than a borrower with a lower LVR. This could make a big difference to your repayments, so it is important to save as much as you can towards a deposit to reduce the size of your loan and try to get your LVR under 80%.’ **

Looking for some tips on creative ways to get into the housing market? Check out our last blog here.

Traditionally, borrowers with LVRs of more than 80%, so with less than a 20% deposit, are often deemed to be stretching their financial resources. APRA has been concerned for some time that the lenders with 90% or even 95% LVR limits are putting borrowers in a tricky situation.

So, what could this mean for you if you are looking for a new loan or an interest-only loan? You might need to provide a larger deposit or look around for a lender with a higher LVR limit.

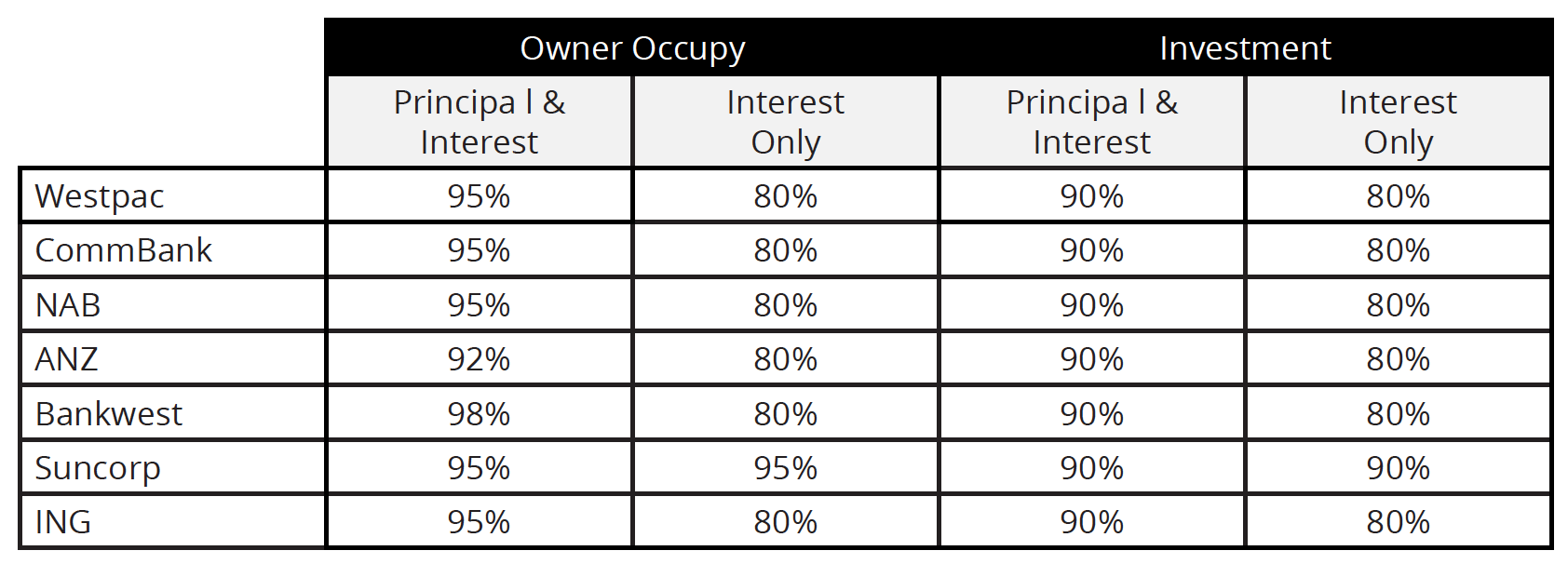

Current LVR limits: As at 23rd June 2017 +

If you have questions about how the changes to LVR limits could affect you – just organise to have a chat with the Oak Financial team.

** https://www.moneysmart.gov.au/managing-your-money/saving/saving-for-a-home

+ Credit Representative 466127 is authorised under Australian Credit Licence 389328

+ LVR limits are subject to lenders policy, terms and conditions, fees and charges and eligibility criteria apply. Lender policy is subject to change at any time without notice.

This article provides general information only and has been prepared without taking into account your objectives, financial situation or needs. We recommend that you consider whether it is appropriate for your circumstances and your full financial situation will need to be reviewed prior to acceptance of any offer or product.